Does Insurance Cover a CPAP Machine? Coverage, Costs, and Requirements

If you’ve been told you might need CPAP therapy, it’s normal to feel overwhelmed by insurance rules. Coverage can feel confusing because it often involves diagnosis requirements, an initial rental period for the device, and adherence (sometimes called compliance) tracking to keep coverage active.

In this guide, you’ll learn when coverage is most common, how Medicare Part B works, what many private plans require, what you might pay out of pocket, and practical ways to reduce the chance of a denial—so you can focus on getting comfortable and staying consistent with therapy.

Quick Answer—When Insurance Usually Covers a CPAP

In many cases, insurance may cover CPAP for obstructive sleep apnea (OSA) when it’s medically necessary and prescribed. So, does insurance cover a CPAP machine? Often yes—when you meet the plan’s criteria and follow its process.

A helpful way to think about coverage is like a short checklist: if one box is missing (no sleep study on file, wrong supplier, missed follow-up), the claim can stall—even when the therapy itself is appropriate.

Requirements vary, but common “must-haves” across many plans include:

- A documented OSA diagnosis (often proven with a sleep study)

- A physician order/prescription for PAP therapy

- Using an approved supplier (especially important with Medicare)

- Proof of early CPAP use (adherence) to continue coverage

These concepts are reflected in Medicare’s PAP coverage criteria and are commonly echoed by private insurers. (See CMS LCD L33718: https://www.cms.gov/medicare-coverage-database/view/lcd.aspx?LCDId=33718 and SleepApnea.org overview: https://www.sleepapnea.org/cpap/does-insurance-cover-cpap)

Bottom line: Most plans may cover CPAP when you meet diagnosis, prescription, supplier, and early-use requirements.

CPAP Basics (and Why It’s Treated as “Durable Medical Equipment”)

What a CPAP machine is (simple explanation)

CPAP stands for continuous positive airway pressure. The machine gently pushes air through a mask to help keep the airway open during sleep. It’s most often used for obstructive sleep apnea, when the airway repeatedly narrows or collapses at night. CPAP doesn’t force you to breathe—it’s more like a soft air “splint” that helps prevent the airway from pinching closed.

Why insurers categorize CPAP as DME

Most insurers classify CPAP devices as durable medical equipment (DME)—similar to items like oxygen equipment or walkers. That matters because DME billing rules often differ from typical prescription-drug benefits.

For example, DME may involve:

- Specific in-network/approved suppliers

- Separate deductibles or coinsurance rules

- Rental-to-purchase arrangements (especially common in Medicare)

Medicare’s coverage criteria for PAP devices fall under DME rules. (CMS LCD L33718: https://www.cms.gov/medicare-coverage-database/view/lcd.aspx?LCDId=33718)

What “PAP therapy” includes (CPAP vs APAP vs BPAP)

You’ll often hear “PAP therapy” used as an umbrella term:

- CPAP: delivers a steady, fixed pressure

- APAP: automatically adjusts pressure within a prescribed range

- BPAP (often called BiPAP): provides different pressures for inhaling vs exhaling; coverage rules may depend on diagnosis details and prior CPAP trial outcomes

Because device types can be covered differently, it’s helpful to confirm what your plan considers medically necessary for your specific diagnosis. (CMS LCD L33718)

Think of PAP as DME with its own supplier and billing rules—learning those rules early saves time and money.

Symptoms and Causes—When a CPAP Is Typically Prescribed (Medical Context)

Coverage decisions often hinge on medical necessity, and medical necessity usually starts with recognizing symptoms and getting tested. These symptoms can suggest sleep apnea, but a sleep study is usually needed to confirm the diagnosis.

Common symptoms that may lead to a sleep apnea evaluation

Many people seek testing after noticing (or being told about) symptoms such as:

- Loud, chronic snoring

- Witnessed pauses in breathing, or gasping/choking during sleep

- Morning headaches, dry mouth, or unrefreshing sleep

- Daytime sleepiness, fatigue, difficulty concentrating (“brain fog”)

- Concerns about blood pressure or heart health (sleep apnea can be associated with cardiovascular risk)

A common scenario is a bed partner noticing breathing pauses first, while the person with OSA mainly feels “tired all the time.” Both types of observations can be important to document.

Common causes/risk factors for OSA

Risk factors can include:

- Airway anatomy (smaller airway, jaw structure)

- Weight changes

- Nasal obstruction or chronic congestion

- Aging

- Alcohol or sedative use (which may relax airway muscles)

When to talk to a clinician about testing

It’s especially important to ask about testing if you have excessive daytime sleepiness, nighttime choking/gasping, or safety concerns such as drowsy driving.

To learn more about testing options, see Home Sleep Test vs Lab Study: Which Sleep Test Is Best for You: https://sleepandsinuscenters.com/blog/home-sleep-test-vs-lab-study-which-sleep-test-is-best-for-you

Symptoms point the way, but a sleep study usually confirms OSA before insurance will consider CPAP coverage.

Medicare Coverage for CPAP (Medicare Part B)

What Medicare Part B covers (in plain language)

Medicare Part B typically covers CPAP therapy for OSA as DME when criteria are met. A key rule: you generally need to obtain the device through a Medicare-enrolled DME supplier for Medicare coverage to apply. (CMS LCD L33718: https://www.cms.gov/medicare-coverage-database/view/lcd.aspx?LCDId=33718)

If you buy equipment outside the required channel, coverage may be denied or limited, even if the therapy itself is otherwise eligible.

Medicare requirements checklist

While individual circumstances vary, common Medicare requirements include:

- A documented OSA diagnosis (usually based on a sleep study)

- A prescription/order for PAP therapy

- Equipment obtained through a Medicare-enrolled DME supplier

If you’re trying to understand how severity is measured and discussed, this primer on the AHI score can help: https://sleepandsinuscenters.com/blog/ahi-score-explained-understanding-your-sleep-apnea-severity

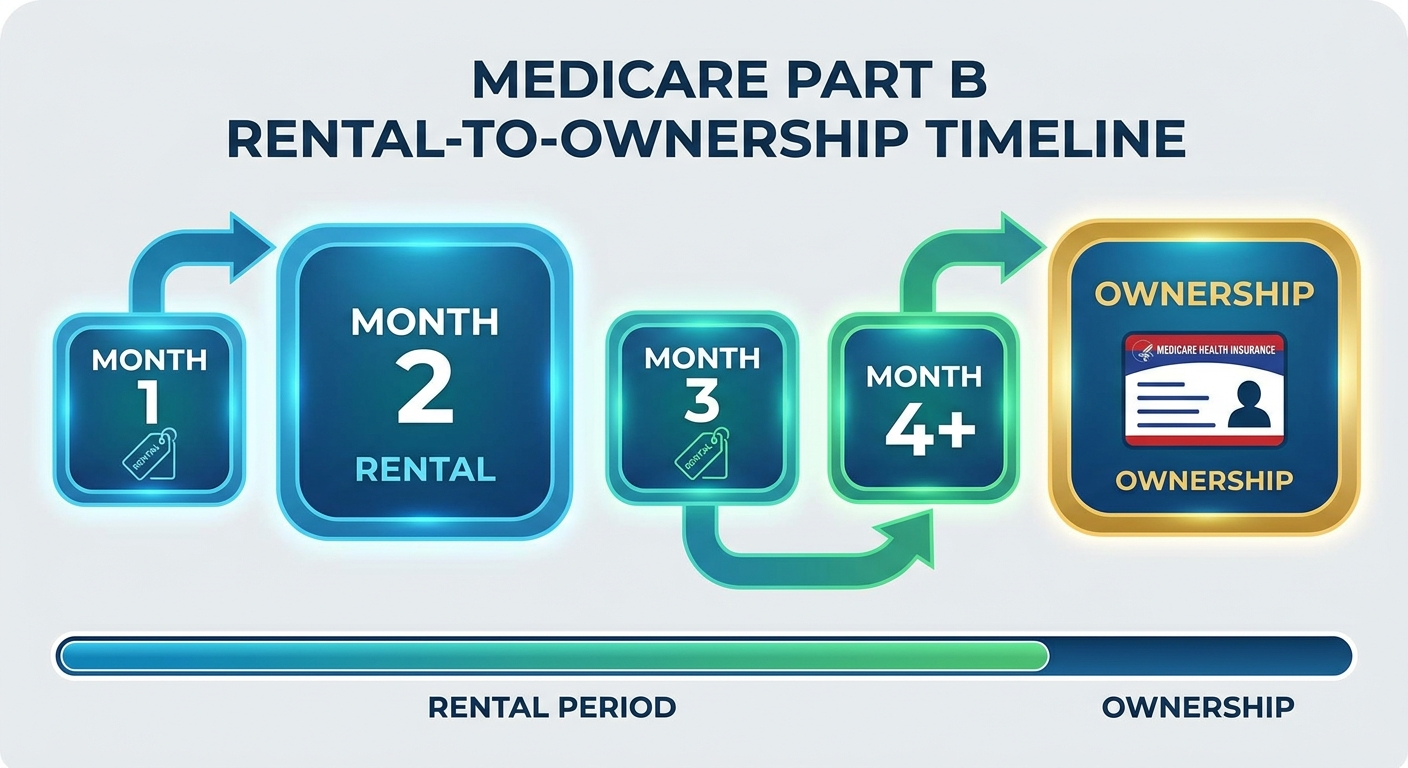

Medicare costs to expect (typical structure)

Medicare cost-sharing often involves:

- A Part B deductible (if not already met for the year)

- Coinsurance (your share of the Medicare-approved amount)

CPAP is often billed first as a rental (with monthly charges) before ownership rules kick in, depending on Medicare policy and continued eligibility. (CMS LCD L33718; CMS decision memo context: https://www.cms.gov/medicare-coverage-database/view/ncacal-decision-memo.aspx?proposed=N&NCAId=204)

For helpful Medicare-oriented summaries, you can also review:

- Humana: https://www.humana.com/medicare/medicare-resources/sleep-apnea-cpap-machine

- UnitedHealthcare: https://www.uhc.com/news-articles/medicare-articles/will-medicare-cover-a-cpap-machine

Medicare adherence rules for continued coverage

Medicare coverage commonly includes an early monitoring period where usage is reviewed. A widely cited benchmark is at least 4 hours per night on 70% of nights during the initial trial period. Medicare’s rule is more specific: beneficiaries typically must demonstrate at least 4 hours per night on 70% of nights during a consecutive 30-day period within the first 90 days, along with a face-to-face re-evaluation in that window documenting benefit and adherence. (CMS LCD L33718)

If you’re struggling in week one, don’t “wait it out.” Early troubleshooting can make the difference between meeting adherence and falling short.

For Medicare, the right supplier plus early, documented benefit are key to keeping coverage active.

Private Insurance Coverage for CPAP (Employer Plans, Marketplace Plans)

What private insurers commonly require

Many private plans cover PAP therapy, but they may require steps such as:

- A sleep study (home or lab) confirming OSA

- Documentation supporting medical necessity

- A prescription and correct diagnosis coding

- Prior authorization (in some plans)

Because policies differ, ask your insurer whether CPAP is covered under DME, whether you need prior authorization, and which suppliers are in-network. (SleepApnea.org: https://www.sleepapnea.org/cpap/does-insurance-cover-cpap)

A quick example question that often saves time: “Do you require a specific DME vendor, and do I need prior authorization before the device is dispensed?”

Adherence monitoring: how it works and why it matters

Private insurers frequently track usage through device data (often transmitted via cellular/Wi‑Fi or downloaded). Commonly tracked items include:

- Hours used per night

- Percentage of nights used

- Mask leak and therapy metrics (varies by device and plan)

Many plans use the same common adherence standard: at least 4 hours per night on at least 70% of nights during the early monitoring period. If adherence isn’t met, coverage for ongoing rental charges or supplies may pause, and you may need follow-up documentation. (Upstate adherence explanation: https://www.upstate.edu/sleep-center/pap/adherence.php)

Check prior authorization and in-network DME rules before your device is dispensed to avoid avoidable denials.

What You Might Pay: CPAP Costs With Insurance vs Without Insurance

Common cost components (easy-to-scan list)

Costs typically come from several pieces, not just the machine:

- Sleep study cost-sharing (home or lab)

- Office visits (evaluation and follow-ups)

- CPAP device charges (often rental first)

- Supplies: mask, cushion/pillows, tubing, filters, humidifier chamber

- Adherence data downloads and follow-up visits (varies)

Why your out-of-pocket cost differs from someone else’s

Even with similar coverage, costs can differ based on:

- Whether your deductible is already met

- Coinsurance percentage vs fixed copays

- In-network vs out-of-network suppliers

- Plan-specific DME rules and “preferred” equipment contracts

This is also where people often ask again: does insurance cover a CPAP machine at 100%? Sometimes it can feel like it doesn’t—when the plan does cover it, but you still owe deductible/coinsurance. A common reaction is: “I thought it was covered—why am I getting a bill?” Often, the answer is that DME is covered, but cost-sharing still applies.

When buying a CPAP out-of-pocket can make sense

Paying cash may be worth considering if:

- You have a high-deductible plan and haven’t met it

- You need treatment quickly while authorization is pending

- You want a backup/travel device (many plans won’t cover a second machine)

For a budgeting-focused overview, see Affordable CPAP Machines: What to Look For: https://sleepandsinuscenters.com/blog/affordable-cpap-machines-what-to-look-for

Even when covered, DME cost-sharing can create bills—ask your DME and insurer for estimates up front.

Step-by-Step: How to Get a CPAP Covered by Insurance (Checklist)

Step 1 — Get evaluated and document symptoms

Share key sleep-related symptoms (snoring, witnessed pauses, daytime sleepiness). Clear documentation supports medical necessity, which is central to coverage. (CMS LCD L33718; SleepApnea.org)

If possible, bring specifics (for example, how often you wake up gasping, or whether fatigue affects work or driving).

Step 2 — Complete a sleep study (home or lab)

Insurers typically want objective evidence of OSA from a sleep test. To compare options, visit: https://sleepandsinuscenters.com/blog/home-sleep-test-vs-lab-study-which-sleep-test-is-best-for-you

Step 3 — Obtain a prescription/order

PAP devices generally require a prescription for insurance coverage and for purchase through many channels.

Step 4 — Use an approved DME supplier

- Medicare: use a Medicare-enrolled DME supplier (a frequent source of denials when missed). (CMS LCD L33718)

- Private insurance: use an in-network/approved supplier when required.

Step 5 — Start therapy and protect your coverage with adherence

Early comfort matters because adherence is often reviewed in the first weeks. Helpful starters:

- Ask about mask refitting if leaks or discomfort are interfering

- Consider humidification if dryness is a barrier

- Schedule follow-ups if you’re struggling early rather than waiting

A little planning around documentation, follow-up, and supplier choice prevents most coverage delays.

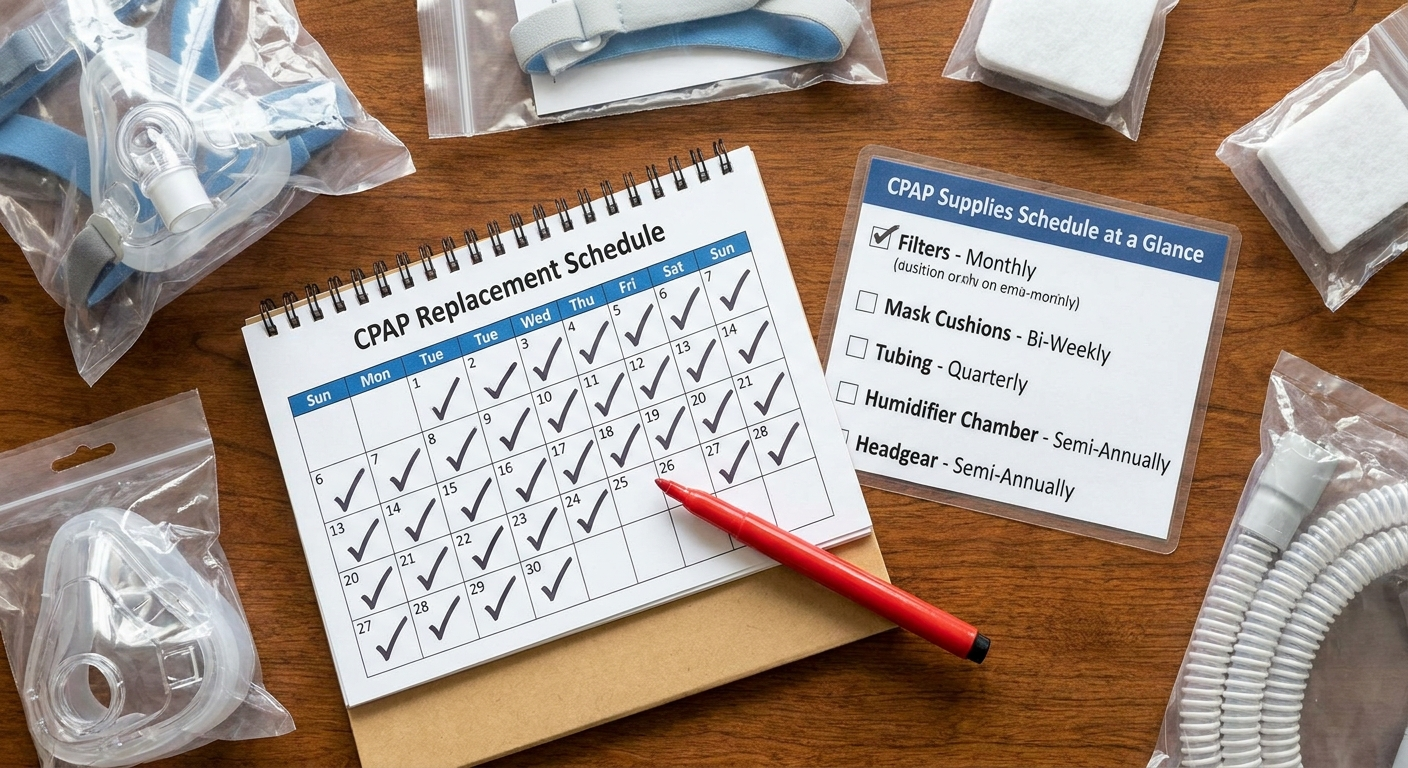

Replacement Supplies: What Insurance Usually Covers (and When)

Common CPAP supplies and why replacement is needed

Supplies wear down with normal use:

- Cushions/pillows can lose their seal

- Filters can clog

- Tubing and water chambers can degrade or crack

When parts wear out, you may notice more leaks or less comfort—both of which can make it harder to meet adherence goals.

Typical replacement schedule (plan-dependent)

Many plans cover supplies on a recurring schedule, but exact timing and cost-sharing vary. Your supplier typically helps track eligibility, but it’s still wise to confirm what your plan allows. (SleepApnea.org)

For a patient-friendly timeline, see When to Replace CPAP Supplies: Essential Timeline for Optimal Therapy: https://sleepandsinuscenters.com/blog/when-to-replace-cpap-supplies-essential-timeline-for-optimal-therapy

How to avoid gaps in supply coverage

- Order through the correct supplier channel

- Keep required follow-up appointments/documentation up to date

- Ask what documentation is needed if you switch masks or devices

Staying on your supply schedule supports comfort, adherence, and uninterrupted coverage.

Treatment Tips (Lifestyle + Comfort) That Help You Stay Adherent

Because insurers often review usage, comfort isn’t just “nice to have”—it can affect whether coverage continues. (Upstate: https://www.upstate.edu/sleep-center/pap/adherence.php)

Make CPAP easier to use (common comfort upgrades)

- Mask fit and sizing: small adjustments can make a big difference in leak and comfort. See CPAP mask sizing: https://sleepandsinuscenters.com/blog/cpap-mask-sizing-guide-find-the-perfect-fit-for-comfortable-sleep

- Humidification for dryness: learn about CPAP humidifier settings: https://sleepandsinuscenters.com/blog/cpap-humidifier-settings-guide-for-optimal-therapy-comfort

- Nasal congestion strategies: addressing congestion can make PAP therapy easier to tolerate (discuss options with a clinician).

Habits that improve OSA outcomes alongside CPAP

General measures often discussed alongside therapy include side sleeping, alcohol moderation near bedtime, weight management support, and consistent sleep timing (your clinician can guide what’s appropriate for you).

Make the first 1–2 weeks as easy as possible—early comfort drives better adherence and better sleep.

Common Reasons Insurance Denies CPAP Coverage (and What to Do)

Missing documentation or wrong supplier

Common administrative reasons include:

- Sleep study or documentation not submitted

- Prior authorization required but not completed

- Using a non-approved supplier (especially a Medicare issue) (CMS LCD L33718)

Not meeting adherence during the trial period

If usage is below the insurer’s threshold, coverage for ongoing rental charges may pause or stop, and you may need additional documentation or re-evaluation to continue coverage. If comfort is the barrier, address mask fit, dryness, pressure comfort, or nasal issues early.

For educational info about ENT-related contributors to CPAP comfort, see ENT Care for People Who Use CPAP Machines: https://sleepandsinuscenters.com/blog/ent-care-for-people-who-use-cpap-machines

Next steps if denied

- Request the denial letter and identify the exact reason

- Ask what documentation is needed (sleep study results, prescription, adherence report)

- Use the plan’s appeal process and submit updated supporting records when appropriate

Find the exact denial reason, close the documentation gap, and appeal with clear supporting evidence.

FAQs

1) Does insurance cover a CPAP machine for mild sleep apnea?

Sometimes. Coverage may depend on how your plan defines medical necessity, your sleep study findings, and your symptoms. Learning how severity is measured can help: AHI score explained https://sleepandsinuscenters.com/blog/ahi-score-explained-understanding-your-sleep-apnea-severity (See also CMS LCD L33718; SleepApnea.org)

2) Do I need a sleep study for insurance to cover CPAP?

Often, yes. Many insurers require objective testing (home or lab) to document OSA and support medical necessity. (SleepApnea.org; CMS LCD L33718)

3) Does Medicare cover CPAP supplies like masks and tubing?

Generally, Medicare covers medically necessary PAP supplies on an allowed schedule, with cost-sharing that depends on your coverage details. (CMS LCD L33718)

4) What is CPAP adherence, and why does it matter for insurance?

Adherence typically refers to using CPAP enough for the insurer to continue paying—commonly at least 4 hours per night on at least 70% of nights during the early monitoring period. (Upstate: https://www.upstate.edu/sleep-center/pap/adherence.php)

5) Can I buy a CPAP online and get reimbursed by insurance?

Sometimes, but it can be difficult. Many plans require specific suppliers, documentation, and billing formats—especially Medicare, which requires Medicare-enrolled DME suppliers for coverage. (CMS LCD L33718)

6) What if I don’t meet adherence—do I lose my machine?

Coverage for ongoing rental charges may pause or stop, and you may need additional documentation or re-evaluation to continue coverage. Early follow-up and troubleshooting can be important. (CMS LCD L33718; Upstate)

7) Will insurance cover a different mask if the first one doesn’t fit?

Often yes, but timing and supplier policies vary. A good starting point is improving fit and seal; see CPAP mask sizing: https://sleepandsinuscenters.com/blog/cpap-mask-sizing-guide-find-the-perfect-fit-for-comfortable-sleep (SleepApnea.org)

Conclusion + Next Steps

So, does insurance cover a CPAP machine? In many cases, yes—but successful coverage usually depends on four pillars: a confirmed diagnosis, a prescription, using the correct supplier, and meeting early adherence requirements. Medicare and private plans often share these themes, even though the paperwork and cost-sharing details differ.

If you’re starting the process, consider scheduling a sleep evaluation and asking your insurer these practical questions:

- Is CPAP covered under my DME benefit?

- Do I need prior authorization?

- What are the rental terms and what will I owe (deductible/coinsurance)?

- What is the adherence monitoring window and required threshold?

To take the next step with Sleep and Sinus Centers of Georgia, book an appointment here: https://www.sleepandsinuscenters.com/

You can also explore testing options here: https://sleepandsinuscenters.com/blog/home-sleep-test-vs-lab-study-which-sleep-test-is-best-for-you

With the right steps, coverage is achievable and sustainable.

Sources

- CMS Local Coverage Determination (LCD) L33718 (PAP devices): https://www.cms.gov/medicare-coverage-database/view/lcd.aspx?LCDId=33718

- CMS Decision Memo (OSA/PAP policy context): https://www.cms.gov/medicare-coverage-database/view/ncacal-decision-memo.aspx?proposed=N&NCAId=204

- SleepApnea.org (insurance overview): https://www.sleepapnea.org/cpap/does-insurance-cover-cpap

- Upstate Sleep Center (adherence explanation): https://www.upstate.edu/sleep-center/pap/adherence.php

- Humana (Medicare CPAP resource): https://www.humana.com/medicare/medicare-resources/sleep-apnea-cpap-machine

- UnitedHealthcare (Medicare CPAP article): https://www.uhc.com/news-articles/medicare-articles/will-medicare-cover-a-cpap-machine

Medical Disclaimer

Medical disclaimer: This article is for informational purposes only and does not provide medical advice. Coverage rules vary by plan and patient circumstances. For diagnosis and treatment guidance, consult a qualified clinician; for benefit details, contact your insurer.

This article is for educational purposes only and is not medical advice. Please consult a qualified healthcare provider for diagnosis and treatment.

Don’t let allergies slow you down. Schedule a comprehensive ENT and allergy evaluation at Sleep and Sinus Centers of Georgia. We’re here to find your triggers and guide you toward lasting relief.